84% of global crypto volume runs through derivatives, not spot markets. That number has held for two years and keeps climbing. Founders scoping exchange scripts in 2026 tend to frame this as a product question — spot, futures, or margin, pick one. But it’s not a product question. It’s an infrastructure question. Each engine has a different architecture, a different failure mode, and a different cost profile. Build the wrong one first, or combine them without the right foundation, and you’re looking at $30,000 to $60,000 in rework before your platform handles real volume. Here’s exactly what each engine requires.

Why the Three Engines Are Architecturally Different

Most articles explain spot, futures, and margin from the trader’s view. You need the builder’s view.

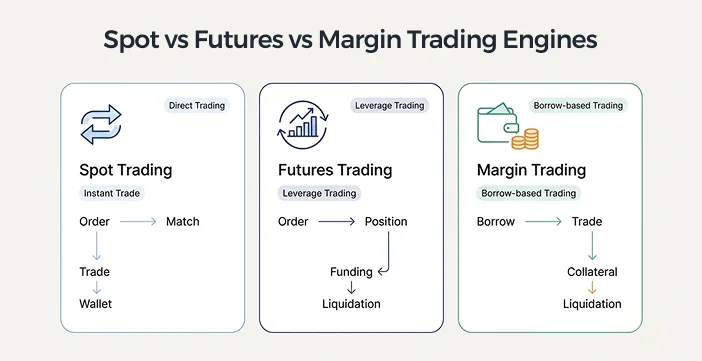

A spot engine’s job is straightforward: match a buy order to a sell order, deduct from one wallet, credit another, done. Settlement is atomic. The engine holds no ongoing state after the trade closes. A Node.js in-memory order book running price-time priority logic can handle 10,000+ matches per second. Once the trade fills, the position is gone.

Futures changes that entirely. When a trader opens a 20x BTC/USDT perpetual, the engine opens a position record and keeps it open — sometimes for weeks. It calculates funding payments every 8 hours, tracks the mark_price in real time, and monitors the margin ratio continuously. The exchange is now in an ongoing contract with that trader. If their margin drops below the maintenance threshold, the liquidation engine must force-close the position within milliseconds.

Margin sits in between. It runs the same order matching as spot, but adds a lending pool, a borrow ledger, and an interest rate tracker. The engine loans funds to the trader, charges interest per hour or per day, and liquidates the collateral if the position health drops below the floor. The matching logic is shared. But the borrow layer and collateral monitor are entirely separate systems with their own database tables and risk calculations.

One team we worked with tried to add margin by bolting a borrowing ledger onto their existing spot database. It worked fine in staging. The first time two margin positions triggered liquidation simultaneously in production, the matching engine deadlocked. They rebuilt the liquidation flow from scratch — 5 weeks of delay and around $16,000 they hadn’t budgeted for. This is what happens when you treat margin as a spot feature instead of a separate engine.

What a Spot Trading Engine Actually Needs

Spot is the foundation. Most white label exchange scripts ship with a working spot engine included. But “working” and “production-ready” are not the same thing.

The core components: an in-memory order book (typically a sorted list indexed by price level), a matching engine running price-time priority, an atomic settlement layer that debits and credits wallets in a single transaction, a fee engine applying maker-taker rates per user tier, and a WebSocket feed pushing real-time book updates and trade history to the front end.

Where spot engines diverge is throughput. A Laravel-based matching engine handles roughly 500 to 1,000 matches per second — fine for a regional launch targeting a few hundred daily active traders. A Node.js or Go-based engine pushes 10,000 to 50,000 matches per second, which is necessary if you plan to attract market makers or any kind of algorithmic flow. The cost difference is real: about $10,000 to $20,000 more for a performance-grade matching core. Worth it if you’re targeting professionals. Skippable if you’re proving product-market fit.

Something competitors rarely cover: you need an accurate mark price oracle even on spot. Without it, your displayed prices are gameable. We’ve seen smaller exchanges get front-run by bots that briefly spiked the last-traded price before a market maker filled the spread on the other side. Pull index data from at least 3 external sources and use a time-weighted average.

For a deeper look at what production-grade performance benchmarks look like and when your architecture needs to move beyond a standard white label base, the institutional-grade trading engine guide covers latency thresholds, colocation considerations, and infrastructure decisions worth knowing before you finalize your design.

Building a Futures Trading Engine: Perpetuals First

Quarterly futures are a phase-two product. Perpetuals are where the volume is, and they should be your first derivatives build. The four sub-systems that make up a futures engine all need to run in parallel — if any one of them lags, your exchange takes on risk it can’t absorb.

Funding Rate: Perpetual contracts need a funding mechanism to keep the contract price anchored to spot. Every 8 hours (standard), longs pay shorts or vice versa depending on whether the futures price is above or below the index. Your engine calculates this using a premium index weighted against external exchange data. Get this wrong and your platform bleeds money to arbitrageurs. One exchange we know of had a buggy funding calculation running for 11 days before anyone caught it. The loss was around $40,000.

Mark Price vs. Last Traded Price: Your liquidation engine must use mark_price, not last_traded_price. Mark price is a weighted average pulled from 3 to 5 external index sources — Binance, OKX, and Bybit are the standard references. If you use last traded price for liquidations, a single large order can briefly push the price and trigger targeted liquidations. This has been exploited on small exchanges multiple times.

Linear vs. Inverse Contracts: Start with linear USDT-margined perpetuals. They settle in USDT, which keeps the P&L math simple and your accounting clean. Inverse contracts — denominated in USD but settled in the underlying crypto — require a separate calculation model and are typically a phase-two addition. Unless you already have strong demand from traders who prefer coin-margined products, build linear first.

The insurance fund is non-negotiable. When a position goes bankrupt — meaning the loss exceeds the trader’s margin — the insurance fund covers the gap before the system triggers auto-deleveraging (ADL). ADL forcibly reduces profitable traders’ positions to cover losses. Most traders don’t know it exists until it hits them, and when it does, they leave. Seed your insurance fund with at least $50,000 to $100,000 in USDT at launch. Replenish it from a portion of trading fees on an ongoing basis.

The Margin Trading Engine: Borrow, Collateral, Liquidation

Margin trading lets traders borrow funds from the exchange to amplify their spot positions. Typical leverage ranges from 3x to 10x — well below futures, which can reach 100x or more. The risk profile is also lower, which makes margin a good middle layer between spot and full derivatives.

The engine needs three layers working together. A lending pool that tracks available funds, who deposited them, and at what interest rate. A borrow ledger that tracks each open loan — the principal, accrued interest, and time-to-repayment. And a collateral health monitor that checks each position’s margin ratio in real time and triggers liquidation when it drops below the maintenance floor.

Cross margin and isolated margin are two different implementations, and you’ll need to decide upfront which to launch. Isolated margin is simpler: the risk is contained to a single position. If it’s liquidated, the rest of the account is untouched. Cross margin lets the full account balance act as collateral across all open positions, which reduces how often liquidations trigger — but it means one bad position can drain everything. Most scripts ship isolated margin first. Cross margin typically adds $10,000 to $18,000 in development and makes more sense once you have traders running multi-position strategies.

The interest rate system isn’t just a risk mechanism — it’s also a revenue stream. Borrowers pay 0.01% to 0.02% per hour on most platforms, depending on the asset and lending pool utilization. That compounds 24/7 across every open borrow position. At scale, margin interest often becomes the second-largest income source on an exchange, right behind trading fees. Don’t underestimate it when modeling your business case.

Order Types Across All Three Engines

You need a shared order layer that works consistently across spot, futures, and margin. The baseline set — limit, market, stop-loss, take-profit, and trailing stop — covers about 90% of what retail traders use. Beyond that, you’re building for professional and algorithmic flow.

Fill-or-Kill (FOK) must execute completely in a single fill or cancel entirely. Useful for large block orders where partial fills create execution risk. Immediate-or-Cancel (IOC) fills whatever it can instantly and cancels the rest. Post-only orders refuse to take liquidity — they only add to the book, which qualifies the trader for maker fee rates. Good-Till-Cancel (GTC) stays open until manually closed or filled, regardless of session.

Each order type needs distinct matching logic and a different path through the settlement layer. A full order type library adds roughly $8,000 to $15,000 to a base exchange script. Don’t build all of them for v1. Launch with limit, market, stop-loss, and take-profit. Add FOK and IOC when you’re ready to target professional traders and market makers.

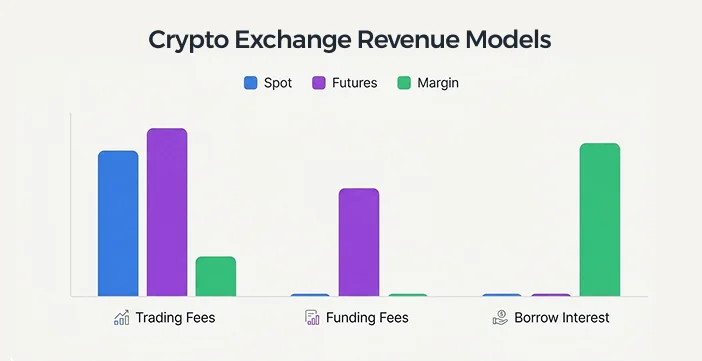

Revenue Models: Maker-Taker, Funding Fees, Borrow Interest

Each trading engine generates different revenue. Understanding the model before you build lets you design the fee layer correctly from the start.

Spot runs on maker-taker fees. Makers — traders who add liquidity to the order book — typically pay 0.01% to 0.1%. Takers pay more, usually 0.05% to 0.15%. At $5M in daily spot volume, that’s $2,500 to $7,500 per day from fees alone. The split between maker and taker determines how attractive your platform is to market makers, who provide the liquidity that makes your order book deep.

Futures generates two revenue streams. First, a per-contract trading fee on each open and close — typically lower than spot at 0.02% to 0.06%. Second, a platform cut of the funding fee flow. When longs pay shorts (or vice versa), the exchange keeps 10% to 20% of the total payment as a platform fee. At significant volume, this becomes meaningful — some exchanges earn 20% to 25% of total revenue from funding fees during high-volatility periods.

Margin interest is the primary income from the margin engine. The exchange earns the spread between what it pays lenders and what it charges borrowers. That spread typically runs 0.003% to 0.008% per hour. Not dramatic per trade. But it runs 24/7 on every open borrow position, with no additional transaction required. Understanding how different exchange script features connect to your launch cost and revenue structure is critical before you finalize which modules to include in your build.

Unified Account vs Separate Accounts

Legacy exchange architecture required separate accounts for spot, margin, and futures. Traders had to manually transfer funds between wallets every time they wanted to switch products. That friction costs you users.

Unified accounts eliminate that. One balance covers all trading modes. The engine tracks sub-ledgers internally for each product type — how much is locked in a margin borrow, how much is posted as futures margin, how much is free — but presents a single balance to the trader. Binance, OKX, and Bybit all run unified accounts, and traders moving from those platforms to your exchange will expect the same.

The technical complexity is real. A unified account requires a cross-product collateral system that understands position-level locks across all three engines simultaneously. Getting this logic wrong means under-collateralized positions — a direct financial risk to the platform. Most white label scripts don’t include a true unified account out of the box. Expect to add $12,000 to $25,000 for this module. It’s worth it for a professional-grade build. Skip it for v1 if you’re launching lean.

Which Module to Launch First

Spot first. No exceptions.

Spot is where you find the bugs in your order matching, your settlement logic, and your fee engine — under real money, real wallets, and real trading behavior. Every bug you catch in spot before adding futures costs 5x less to fix than the same bug discovered in a derivatives system with position management and liquidation logic running on top.

Launch margin second, if your target users are retail traders who already understand crypto markets. Margin adds meaningful revenue without requiring an entirely separate position management system. The borrow/lend layer is complex, but it doesn’t introduce the same risk surface as a full futures engine.

Futures third — but only once your spot and margin engines are stable and you’re seeing at least $1M to $2M in daily spot volume. Futures needs liquidity to work properly. Without enough volume, the funding rate misfires, the order book is too thin for real traders, and your insurance fund gets stress-tested before it’s had time to grow.

The mistake we see constantly: founders building all three at once because they want to compete with Binance on day one. One platform we worked with launched futures before their spot engine had processed 30 days of live trading. A bug in the liquidation engine incorrectly closed a test user’s position. They halted futures for 3 weeks to audit the codebase. The trust damage cost more than the fix.

Build in sequence. Get spot right. Add margin. Add futures. Each phase funds the next, and each one teaches you something about how your users trade — information you need before designing the next engine.

Frequently Asked Questions

What’s the technical difference between a spot engine and a margin trading engine?

A spot engine matches orders and settles them immediately — it holds no ongoing state once a trade closes. A margin engine runs the same order matching, but adds a borrow/lend layer on top: the exchange loans funds to the trader, tracks interest accrual in real time, and monitors the collateral ratio continuously. If the ratio drops below the maintenance floor, an automated liquidation closes the position. The matching logic is shared; the borrow ledger and health monitor are separate systems with their own database tables and risk calculations.

How much does it cost to build a futures trading engine from scratch vs. using a white label script?

A custom-built futures engine with full position management, funding rate logic, mark price feeds, liquidation automation, and insurance fund logic costs between $80,000 and $250,000 and typically takes 6 to 12 months. A white label exchange script with futures support brings this down to $40,000 to $120,000 and cuts time to market by 60% to 70%. Most serious founders start with white label and invest in custom development once they hit $5M or more in monthly trading volume and have a clear picture of where the base script is limiting them.

Do I need an insurance fund on my futures exchange, and what size should it be?

Yes, from day one. The insurance fund absorbs losses when a trader’s position goes bankrupt — meaning their margin is wiped before the position can close at break-even. Without it, the exchange either absorbs the loss directly or triggers auto-deleveraging (ADL), which forcibly reduces profitable traders’ positions. Both outcomes damage platform trust. Most launch-stage exchanges seed the fund with $50,000 to $100,000 in USDT and replenish it with a percentage of futures trading fees on an ongoing basis.

What’s the difference between linear and inverse futures contracts?

Linear contracts (USDT-margined) are settled in USDT. A BTC/USDT perpetual at 10x leverage pays profits and losses in USDT, regardless of where Bitcoin is priced. Inverse contracts are denominated in USD but settled in the underlying crypto — a BTC/USD perpetual pays out in BTC. Linear contracts are significantly simpler to implement and should be your first build. Inverse contracts require a different P&L calculation model and are typically added in phase 2 once you know there’s demand for them from your user base.

Can one exchange script codebase support spot, futures, and margin?

Yes, but the architecture has to be designed for it from the start. All three engines share the same user account system, wallet infrastructure, and KYC/AML layer. The order matching, position management, and risk logic run as separate modules communicating through internal APIs. A properly structured exchange script uses a unified account layer with product-specific sub-ledgers. Retrofitting futures or margin onto a spot-only codebase after launch is expensive — expect $20,000 to $50,000 in rework depending on how tightly the original system was built.

How does the funding rate generate revenue for my exchange?

The funding rate is a periodic payment exchanged between long and short holders on perpetual futures — typically every 8 hours — designed to keep the futures price anchored to spot. When one side pays the other, the payment flows through your exchange. Most platforms keep 10% to 20% of that total flow as a platform fee. At high volume, this compounds into meaningful revenue: some exchanges earn 20% to 25% of total platform income from funding fees during high-volatility market conditions.

Should I launch with cross margin or isolated margin first?

Isolated margin first. It’s simpler to implement and limits risk to a single position — if it liquidates, the rest of the account is unaffected. Cross margin shares the full account balance as collateral across all open positions, which reduces how frequently liquidations trigger but requires a cross-product collateral engine that can handle simultaneous position health calculations across multiple pairs. Most white label scripts include isolated margin by default. Cross margin is typically a $10,000 to $18,000 add-on and makes more sense once you have users running multi-position strategies.