Seventy percent of new crypto exchanges don’t make it past 18 months. The most common reason isn’t a bad UI or weak marketing. It’s execution failure — trades that don’t fill, spreads that widen on busy days, order books that look populated but can’t handle a $10,000 market order without significant slippage. All of that traces back to one problem: no real liquidity infrastructure.

External liquidity API integration is how you fix it. Instead of waiting years to build organic depth, you plug your exchange into institutional order books from providers like B2Broker or AlphaPoint and route your users’ trades through that depth from day one. This guide covers what the integration actually looks like at a code and architecture level, so you know what you’re signing up for before you start.

What a Liquidity API Actually Does

Three API types get confused here, and conflating them costs founders weeks of rework.

A Market Data API gives you read-only price feeds. You can power charts, display tickers, build a price alert system. But the prices aren’t executable. You’re looking at what the market is doing, not actually participating in it.

A Trading API lets users submit orders on your own exchange. It presumes your platform already has the liquidity to match those orders on both sides of the book. At launch, that depth doesn’t exist.

A Liquidity API is the piece that bridges the two. It connects your matching engine to external order books held by institutional providers. When a user places a buy order, your system queries the LP API for an executable quote, gets a fill price, and completes the trade — in milliseconds and without the user knowing there’s an external rail under the hood.

One team built an exchange over eight months, integrated a solid market data feed, and called it “connected to liquidity.” When they opened for real trading, their order book showed prices but had no counterparty depth to match against. They paused trading for two weeks to fix the architecture. Two weeks after launch is not when you want to go dark.

The distinction matters before you write a line of integration code. Make sure your LP agreement is specifically for executable quotes, not market data. Read the contract carefully on this point.

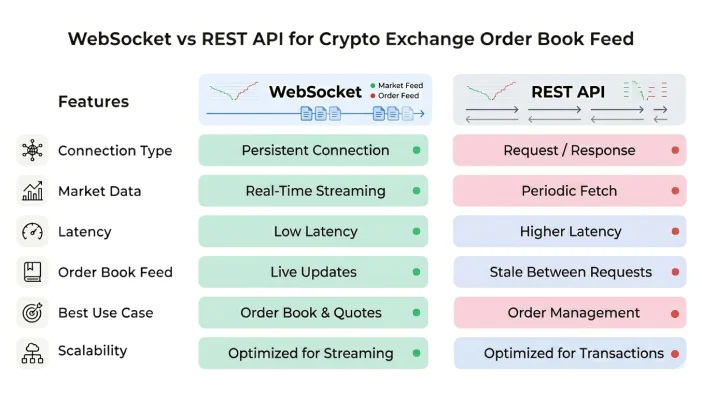

WebSocket vs REST: Which Feed to Use

Most liquidity providers offer both, and you’ll use both — just for different things.

REST is for discrete operations: place an order, cancel an order, check account balance, pull trade history. It’s stateless, easy to debug, and straightforward to implement. In Node.js, a signed REST call to a provider like B2Broker is a plain axios.post with three custom headers. Nothing exotic.

WebSocket is for streaming. Live order book updates, executable quote feeds, real-time trade confirmations. The connection stays open and the LP pushes data to you as market conditions change. For your order book display and quote engine, this is non-negotiable.

If you’re polling a REST endpoint every 500ms for price updates instead of maintaining a WebSocket subscription, you’re already serving users stale data. During high-volatility periods when the order book moves 15 to 20 times per second, a 500ms poll means users see prices that are 7 to 10 ticks behind reality. That’s where ghost-price complaints come from — users clicking on a price that’s already moved.

The practical setup: WebSocket for your live depth and quote feed, REST for order management. Some teams try to run a WebSocket-only architecture to keep things uniform. It sounds clean, but reconnect handling during market stress becomes its own engineering problem. Keep the two channels separate and purpose-built.

In Laravel, you’d handle the WebSocket subscription in a background job via php artisan queue:work, with a dedicated Redis channel that your order book service reads from. In Node.js, a ws client with a reconnect loop covers the same ground cleanly.

How to Authenticate with an LP API

Every institutional LP worth connecting to uses HMAC-SHA256 request signing. Plain API keys in a header without a signature are a sign of a provider that hasn’t thought hard about security. Don’t take that as a positive.

Here’s the standard signing pattern in Node.js:

const crypto = require('crypto');

function signRequest(apiSecret, timestamp, method, path, body = '') {

const payload = `${timestamp}${method.toUpperCase()}${path}${body}`;

return crypto

.createHmac('sha256', apiSecret)

.update(payload)

.digest('hex');

}

Your outgoing request carries three headers: API-Key (your public key), Timestamp (current Unix time in milliseconds), and Signature (the HMAC output). The LP reconstructs the same payload using your stored secret and rejects any request where the signatures don’t match.

Three things that trip up integration teams consistently:

Clock drift. If your server’s system clock is off by more than 5 seconds from UTC, the LP rejects requests silently with no useful error message. Enable NTP sync on every server that touches the LP API. This is a 10-minute fix that prevents hours of debugging.

Body serialization order. Some LPs require JSON keys in your request body to be sorted alphabetically before signing. If you serialize the body one way and sign it another, validation always fails. Read the LP’s signing documentation in full — not just the code samples, the full spec.

Key scope. Most providers let you issue multiple API key pairs with different permission scopes. Use a separate key pair for market data access, order management, and any admin-level calls. If one key gets compromised, you revoke it without interrupting everything else.

Store keys in environment variables. In Laravel, that’s .env + config() and nothing stored in the repository. In Node.js, dotenv works fine for staging; for production, pair it with AWS Secrets Manager or HashiCorp Vault. API keys for a live exchange carry the same sensitivity as database credentials.

Single LP vs Multi-LP Aggregation

New exchanges almost always start with a single liquidity provider. That’s the right call for most teams. The question is whether you know the difference between doing it intentionally versus accidentally locking yourself in.

A single LP keeps everything manageable: one set of documentation, one authentication implementation, one support relationship to manage, one WebSocket connection to maintain. Providers like B2Broker and AlphaPoint cover 30 to 50 trading pairs with institutional-grade depth, which handles most startup exchange requirements. Monthly costs typically fall between $2,000 and $6,000 depending on your committed volume and asset classes.

Multi-LP aggregation means pulling order books from two or more providers, normalizing their different schemas into a unified format, and presenting a composite best-bid/best-offer to your users. You also need smart order routing logic that decides, per trade, which LP gets the order based on current depth and fill probability. Tighter spreads, better fill rates, no single point of failure — at the cost of significant engineering work.

Learn how to bootstrap your exchange’s liquidity beyond just API connections once the technical rails are in place.

We’ve seen startups plan multi-LP aggregation from day one and burn through runway before they ever opened for trading. The normalization layer and routing logic alone took one team four months to stabilize. Start with a single LP. Reassess at $500,000 in monthly trading volume, when you can actually measure where you’re losing spread and which pairs need deeper support.

The one exception: if your exchange targets exotic or low-volume pairs that a single institutional LP won’t cover, you may need a second specialist provider for those assets from launch. That’s a targeted two-LP setup, not full aggregation, and it’s manageable without blowing the engineering timeline.

Handling Rate Limits and Failover

LP APIs throttle requests. Typical limits are around 100 REST calls per 10 seconds per API key, with WebSocket sessions timing out after 30 to 60 seconds of inactivity if you don’t send keepalive pings. Exceed the REST limit and you get 429 responses. Repeat offenses can get your IP temporarily banned at the provider’s firewall level.

In Node.js, a token bucket rate limiter using bottleneck keeps you inside limits without manual counting across your application:

const Bottleneck = require('bottleneck');

const limiter = new Bottleneck({ maxConcurrent: 5, minTime: 100 });

const result = await limiter.schedule(() => placeOrder(params));

The bigger risk is provider downtime. LPs do go offline. Not often, but they tend to go down during high-volatility periods when your trading volume is spiking — exactly the moment you can least afford it. Your failover logic needs to handle this before it happens, not after.

A two-tier fallback handles most cases:

- WebSocket disconnects — trigger an immediate reconnect with exponential backoff (start at 1s, cap at 30s, max 5 attempts before escalating)

- WebSocket reconnect fails after 90 seconds — switch order routing to REST polling at 1-second intervals

- REST calls return 503 errors for more than 60 consecutive seconds — pause new order intake and show users a maintenance message

One exchange we know skipped the REST fallback tier. During an LP infrastructure event, their WebSocket went down and their system had no secondary channel. They silently served stale prices for 14 minutes. Several users traded against prices that were 4% off. The exchange covered the difference out of their operating balance — about $22,000 in a single incident.

Build the fallback before launch, even if you never need it.

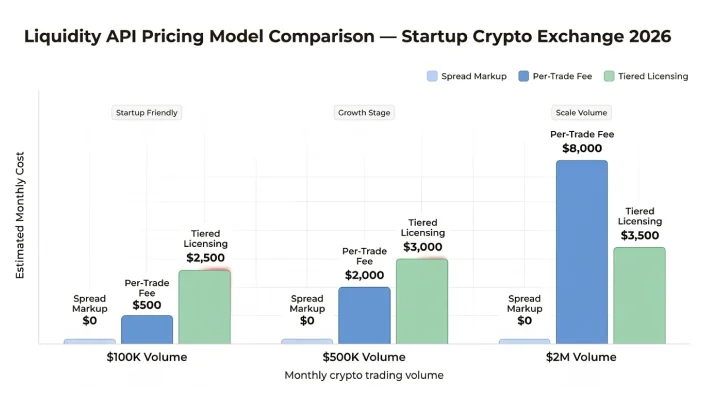

Liquidity API Pricing Models You’ll Actually Encounter

LP pricing comes in three main structures, and the right choice depends on your expected volume.

Spread markup: The LP quotes you a tighter internal price and adds a markup before your users see it. You earn the difference between the internal and displayed spread. This looks like a “free” model but you’re giving up spread revenue you could otherwise control and optimize yourself.

Per-trade fee: A flat fee applied per executed trade. Typical range is $0.10 to $0.50 per trade depending on asset class, trade size, and volume tier. Predictable and easy to model in your unit economics.

Monthly licensing plus volume tier: A base retainer — usually $2,000 to $3,500 per month — plus a per-trade rate that drops as your monthly volume grows. Common with institutional providers like B2Broker and Leverate. The base fee gets you priority support and a dedicated account manager, which matters when something breaks at 2am.

| Pricing Model | Best For | Approximate Cost | Control Level |

|---|---|---|---|

| Spread Markup | Under $1M monthly volume | No fixed fee | Low — LP sets the markup |

| Per-Trade Fee | Mid-volume, predictable trades | $0.10 – $0.50 per trade | Medium — fee is fixed |

| Monthly Licensing + Tier | $1M+ monthly volume | $2,000 – $3,500/month base | High — tiered rate control |

For a startup exchange under $1 million in monthly trading volume, the spread markup model typically works out cheapest because your per-trade count is low and the monthly retainer on the licensing model doesn’t justify itself yet. Past $5 million monthly volume, the tiered licensing model usually wins on total cost. Model both scenarios in a spreadsheet before signing anything — LP contracts run 12 to 24 months.

Testing Before You Go Live

Every serious LP offers a sandbox or demo environment that mirrors their production API with simulated market data. Use it. Every team that skips sandbox testing finds their bugs in production, which is a significantly more expensive debugging environment.

Your pre-launch checklist:

- Order placement and cancellation across all supported trading pairs — confirm fill confirmations come back with the correct fields your order management system expects

- WebSocket reconnect — manually kill the connection and verify your application recovers and resubscribes within the expected window

- Rate limit handling — intentionally fire requests above the limit and confirm your system queues gracefully instead of erroring out with unhandled exceptions

- HMAC rejection — send a deliberately wrong signature and confirm the LP returns the expected 401, not a 500 or silent timeout

- Slippage measurement — place large notional orders in sandbox and compare fill price to the quoted price to understand how depth behaves at your target trade sizes

- Failover trigger — simulate LP downtime by blocking the outbound connection from your application server and confirm the REST fallback kicks in within your defined timeout window

Run this against a staging environment that matches your production configuration exactly — same instance type, same network setup, same Node or PHP version. One team skipped the staging environment for “a quick configuration check” in production. They placed an unintended live order for 2.1 BTC at market. It filled in 400ms. The LP had no undo button.

Frequently Asked Questions

What’s the difference between a liquidity API and a trading API?

A trading API lets users place orders on your exchange. A liquidity API connects your exchange to external order books so there’s actual depth to fill those orders against. You need both — the trading API handles the user-facing side, the liquidity API handles the sourcing of executable quotes from the market.

How long does liquidity API integration typically take?

For a single LP with REST and WebSocket, plan for 4 to 8 weeks of development including testing and sandbox validation. Multi-LP aggregation with order routing logic takes 3 to 5 months depending on your team’s experience with financial systems.

Which liquidity providers work for small startup exchanges?

B2Broker, AlphaPoint, and Deltastock work with startups that can meet minimum monthly volume commitments, usually between $100,000 and $500,000. Institutional desks like B2C2 and Cumberland typically require $5 million or more in monthly volume before onboarding a new client.

Do I need HMAC authentication for all LP APIs?

Any institutional LP worth using requires HMAC-SHA256 signing for private endpoints. Providers that accept plain API keys without signatures are running below-standard security practices. Use HMAC from the start regardless of what a provider technically allows.

What’s a realistic first-year budget for liquidity API integration in 2026?

Budget $2,000 to $6,000 per month for the LP relationship, 4 to 8 weeks of development at your team’s rate, and ongoing infrastructure for the WebSocket connection management layer. Total first-year cost for a lean startup build runs roughly $80,000 to $140,000 all-in.

How do I reduce slippage on my exchange?

Deeper order books reduce slippage. Short-term: connect to a provider with strong depth in your core pairs. Medium-term: add a second LP for your highest-volume pairs. Also configure your routing so large orders are split into smaller child orders — most institutional LPs support this at the API level.

WebSocket or REST for the order book feed?

WebSocket. REST polling introduces latency and puts avoidable load on your servers and the LP’s API. Use WebSocket for live depth and quotes, REST for order management and account operations. The two channels serve different purposes — don’t try to consolidate them.