Most crypto exchanges don’t fail because of bad code. They fail because no one’s trading on them. One founder we worked with launched a well-built platform with 12 supported pairs, solid UI, and zero liquidity strategy. Within 8 weeks, user retention hit 3%. Not because the product was broken. Because every trade slipped 1.5% and spreads looked embarrassing next to Binance.

Liquidity isn’t a feature you add later. It’s the product. This guide walks through exactly how to go from an empty order book to a market that actually works.

Why Liquidity Kills New Exchanges

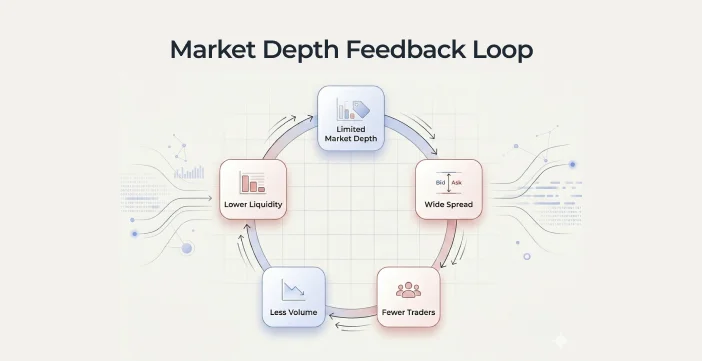

Thin liquidity doesn’t just hurt user experience. It poisons growth.

When a user sees a 2% spread on a BTC/USDT pair, they don’t file a support ticket. They go to Binance. And they don’t come back. Price slippage on larger orders compounds this: a $10,000 ETH trade that slips 0.8% costs that user $80 they didn’t budget for. One experience like that, and they’re gone permanently.

Here’s what’s counterintuitive: the problem feeds itself. Low liquidity means fewer trades. Fewer trades mean fewer fees. Fewer fees mean less money to attract market makers. It’s a spiral that’s genuinely hard to break once it sets in, usually by month 3. We’ve seen this exact pattern destroy exchanges that launched with $2M+ in initial funding.

The goal isn’t to look liquid. It’s to actually be liquid, at least on the pairs that matter.

The Cold Start Problem: What Day 1 Actually Looks Like

Every new exchange faces the same fundamental issue: no users without liquidity, no liquidity without users.

There’s no elegant solution. But some approaches work far better than others.

On day one, you won’t have organic flow. Acknowledge that now and plan around it. What you need on launch day isn’t 200 trading pairs. It’s 3 to 5 pairs with credible depth. BTC/USDT, ETH/USDT, and 1 or 2 pairs specific to your target audience are enough to start. Depth on a handful of pairs beats shallow coverage across 50.

One exchange we worked with launched with 40 pairs because they thought variety would attract users. Their BTC/USDT spread ran at 0.6% on launch day. A competitor launched 2 weeks later with 5 pairs and a 0.04% spread on BTC/USDT. Guess which one grew. Focused always wins early.

Target a bid-ask spread under 0.08% on your top pair before you market to anyone. That’s your minimum viable liquidity bar, and it’s non-negotiable.

Market Makers vs Liquidity Providers: Don’t Confuse Them

These two terms get used interchangeably. They’re not the same thing.

A liquidity provider aggregates order flow from multiple external sources, typically from major exchanges like Binance, OKX, or Kraken, and streams it into your order book via API. They bring depth passively. You pay for the connection through a monthly API fee or a spread markup, and your order book reflects live prices from markets elsewhere.

A market maker actively quotes both sides of a trade on your platform. They carry inventory risk. They’re watching your order book in real time and adjusting quotes based on volatility, flow toxicity, and their own risk parameters. They’re not piping in prices from somewhere else. They’re actually making the market on your exchange.

For a new exchange, you typically need both. Start with a third-party liquidity provider to establish base depth quickly, often within 48 to 72 hours of API integration. Then layer in a market maker to improve spread quality and add responsiveness. Budget $8,000 to $25,000 per month for a reputable market maker. Firms like Wintermute, Kairon Labs, and GSR operate at this range. Anything below $5,000/month and you’re getting a service that’s not actively managing your book.

How to Bootstrap Liquidity in the First 90 Days

Think of the first 90 days in three phases.

Phase 1 (days 1 to 30): Seed the order book. Plug in a liquidity aggregator API to establish base depth on your top pairs. Your Node.js backend handles the WebSocket connections for real-time order book data. Keep pairs narrow. Set spread bands manually if needed. The goal here isn’t volume; it’s credibility. A user who lands on your exchange and sees a 0.05% spread trusts it.

Phase 2 (days 31 to 60): Sign your market maker. Get quotes from at least three firms. Key terms to negotiate: minimum order book depth near mid (how much depth you need within 0.1% of the mid price), response time commitments, and uptime SLAs. Most founders skip the depth-near-mid requirement. Don’t. A market maker can technically post orders 3% away from mid and satisfy a loose contract. Specify depth within 0.1% of mid explicitly in the agreement.

Phase 3 (days 61 to 90): Measure organic flow. What percentage of your 24h volume is coming from non-market-maker accounts? Target 15% organic flow by day 90. If you’re under 10%, your user acquisition strategy needs work, not your liquidity setup.

For building the right foundation from the start, working with an experienced crypto exchange development platform that includes market maker API integration and configurable order book infrastructure saves you 3 to 4 months of engineering work.

Fee Structure as a Liquidity Tool

Most exchanges treat fees as a revenue line. Treat them as a liquidity tool first.

The maker-taker model exists for a reason. Makers (those who add orders to the book) receive a rebate or pay a lower fee. Takers (those who fill existing orders) pay more. A typical structure: makers pay 0% to -0.01% (a rebate you pay them) and takers pay 0.05% to 0.10%. The rebate directly subsidizes market makers and encourages organic users to post limit orders, which thickens your book over time.

One client ran a flat 0.1% fee on both maker and taker for their first 6 months. Their order book never deepened. They switched to 0% maker / 0.08% taker, and within 45 days, depth within 0.5% of mid doubled. Revenue dropped short-term. Volume grew 3x over the next quarter, and total fee income ended up higher. The short-term sacrifice was worth it.

Running zero-fee or negative-fee promos for your top 10 market makers during the first 90 days is a legitimate strategy. Exchanges like dYdX used exactly this approach in their early growth phase.

CEX vs DEX Liquidity Strategies

The playbook differs significantly depending on what you’re building.

On a CEX, you control the order book directly. You can integrate with market makers, configure spread bands through your matching engine, and use your Node.js or Laravel backend to push real-time depth data to users. The challenge is custody: you hold user funds, which creates trust requirements and regulatory obligations.

On a DEX, liquidity lives in smart contracts. You’re not running a traditional order book; you’re managing liquidity pools. Protocols like Uniswap use the constant product formula (x * y = k) to price trades automatically. Curve optimizes for stable pairs with a different bonding curve that keeps slippage near zero for stablecoins. Balancer supports multi-asset pools with custom weights, useful for token launches where you want controlled price discovery.

For a hybrid exchange or a new DEX, liquidity mining works: you pay out your native token as a reward to users who deposit funds into your pools. It attracts capital fast. But it comes with a problem worth its own section.

CEX liquidity scales with capital. DEX liquidity scales with incentives. Both paths work, but they need completely different infrastructure and risk management approaches.

The Mercenary Capital Trap

Liquidity mining attracts capital fast. That’s the appeal. And it’s also the problem.

Mercenary capital describes funds that enter a liquidity pool purely to farm token rewards, with no loyalty to your platform. The moment your emission rate drops or a competitor offers higher APY, that capital exits. In one day. We’ve seen exchanges lose 60% to 70% of their TVL (total value locked) within 72 hours of reducing rewards, taking spreads from 0.04% back to 0.9% overnight. The exchange looked healthy on paper the week before. Then it didn’t.

The fix isn’t to never run mining incentives. It’s to design them properly and build organic demand in parallel.

Run liquidity mining incentives for a capped 90-day window. Require a minimum lockup of 14 to 30 days to qualify for full rewards. Use that window to acquire traders who actually want to use the platform, not just park capital. By the time incentives wind down, you need enough real trading volume that the market maker has reason to stay. If your organic flow is still near zero when rewards expire, the liquidity evaporates, and recovery is much harder the second time around.

Sustaining Liquidity Through Bear Markets and Unlock Events

Liquidity management doesn’t stop at launch. Two situations reliably break exchanges that didn’t plan for them.

Bear markets. Trading volumes drop across the industry during downturns, sometimes by 60% to 80% from peak. Your market maker’s profitability shrinks as spread capture falls. Some will widen spreads significantly or exit contracts altogether. Budget 3 to 6 months of market maker fees in stablecoins before launch. That reserve lets you renegotiate from a position of strength rather than desperation when the market turns.

Unlock events. When a project’s locked tokens become tradeable, the market often reacts sharply. If you’re listing a token with a large unlock approaching, prepare in advance: increase depth near mid 48 hours before the event, pre-coordinate with your market maker on adjusted spread bands, and consider temporarily widening your taker fee slightly to slow order execution. Binance and Coinbase both adjust their market making posture around major unlocks. You should too, even at smaller scale.

Off-peak liquidity is the last piece most founders overlook. Your exchange’s 3am UTC order book might look half as deep as noon. Set minimum depth SLAs in your market maker contract that apply specifically to off-peak hours. Without this clause, the agreement protects your peak hours only, and users trading at odd hours see a completely different exchange.

Sustainable crypto exchange liquidity isn’t one decision. It’s a system you build, test, and adjust over months.

Frequently Asked Questions

How much capital do I need to bootstrap liquidity on a new crypto exchange?

Budget $30,000 to $80,000 for your first 90 days. This covers a market maker retainer ($8,000 to $25,000/month), liquidity aggregator API costs ($500 to $2,000/month), and initial maker-fee rebates. If you’re also running mining incentives on a DEX layer, add $20,000 to $50,000 in native token rewards depending on your target TVL.

What’s the difference between a liquidity provider and a market maker for a new exchange?

A liquidity provider streams external order flow into your book via API. That’s passive. A market maker actively posts two-sided quotes on your platform, carries inventory risk, and adjusts in real time. New exchanges need both: the provider for speed of setup, the market maker for quality of depth.

How do I know if my exchange has enough liquidity?

Watch three numbers: bid-ask spread on your top pair (target under 0.1%), 24h trading volume (aim for $500K minimum), and order book depth within 0.5% of mid price (at least $50K on each side for BTC/USDT). If all three are healthy, you’re in a defensible position.

What is mercenary capital and why does it hurt an exchange?

Mercenary capital is liquidity attracted purely by yield incentives, with no inherent interest in your platform. When rewards drop, it exits immediately. Exchanges that rely on it without building organic trading flow in parallel end up in worse shape when incentives end than before they started.

Should I launch with a CEX or DEX model for better liquidity?

For founders with a market maker budget of $10,000+/month, a CEX gives more direct control over spread quality. For teams without that capital, a DEX with AMM pools lets you bootstrap with user-deposited funds. Hybrid models are possible but add significant engineering complexity that can push your launch back 3 to 6 months.

How do I protect liquidity during a bear market?

Hold 3 to 6 months of market maker fees in stablecoins before launch. Negotiate market maker contracts with explicit off-peak depth commitments. Focus on profitable high-volume pairs rather than trying to maintain a long tail of illiquid listings.

What fee structure works best for attracting market makers early on?

Start with 0% maker / 0.05% to 0.08% taker. For your top 3 to 5 market makers, offer a negative maker fee (a rebate of 0.005% to 0.01% per trade) for the first 90 days. It compensates them for the risk of making markets on a low-volume platform, and it pays for itself once volume picks up.