About 70% of crypto exchanges that launch without a liquidity plan don’t survive past 18 months. The product isn’t always bad. The team isn’t always inexperienced. The problem is usually the same: a user places a $5,000 BTC order on day three, gets 3% slippage, and never comes back. And they tell other people.

Thin order books don’t just hurt trading experience. They kill word of mouth before your exchange has any momentum to protect.

This guide covers the real mechanics of crypto exchange market making for founders: fee structures, market maker agreements, bot infrastructure, and how to get genuine depth on day one without spending $500,000.

Why Thin Order Books Kill New Exchanges Before They Start

The cold start problem in crypto exchange liquidity is straightforward and brutal. Your exchange opens with zero trading history, zero volume, and zero market makers. Traders don’t show up because there’s no liquidity. Market makers don’t show up because there are no traders. You’re stuck in a loop that doesn’t break itself.

One exchange launched in Q3 2024 with a solid CLOB matching engine, a clean UI, and a decent early user base from a referral campaign. By week two, their BTC/USDT spread was sitting at 1.2% on a good day. Binance runs the same pair at around 0.01%. Users deposited, tried one trade, and left. Volume peaked at $180,000 in week one and fell to $12,000 by week four. The platform wasn’t broken. The order book was.

A thin order book signals distrust. Spreads wider than 0.5% on major pairs tell traders the exchange can’t handle meaningful order size. A $20,000 market order hitting a book with only $8,000 of depth within 1% of spot will move the price noticeably against the user. That’s not a software bug. It’s what happens when there aren’t enough resting orders to absorb the trade.

The fix isn’t moving faster or marketing harder. It’s planning your liquidity infrastructure before you write a line of matching engine code.

The Maker-Taker Fee Model: Your First Liquidity Lever

Before approaching any market maker, get your fee model right. It’s the single biggest signal an exchange sends to professional liquidity providers, and most founders get it wrong by playing it too safe.

The maker-taker model charges traders differently based on whether they add or remove liquidity. Makers post limit orders that sit in the book and wait to be filled. Takers fill those orders with market orders. The setup that actually attracts professional activity in 2026 runs from -0.01% to -0.025% for makers (a rebate you pay them) and 0.06% to 0.1% for takers.

Most new exchanges set both sides at a flat 0.1% to keep things simple. That’s a mistake. When a market maker chooses between posting on your exchange at 0.1% cost versus posting on Bybit at a rebate, they pick Bybit every time. You’re competing for capital that has better options, and a flat fee tells professional firms you haven’t thought about that competition.

The structure that works for a new exchange: set maker fees at -0.01% and taker fees at 0.08%. Yes, you’ll run slight negative revenue on maker activity in the early months. That’s the cost of seeding your book. Once daily volume scales past $5 million to $10 million, taker revenue covers it comfortably. Also tier your fees. Market makers who commit to $500,000 or more in daily posted orders get better rebates. This turns your fee schedule into a retention mechanism, not just a cost table.

Market Maker Agreements: What Wintermute and GSR Actually Need

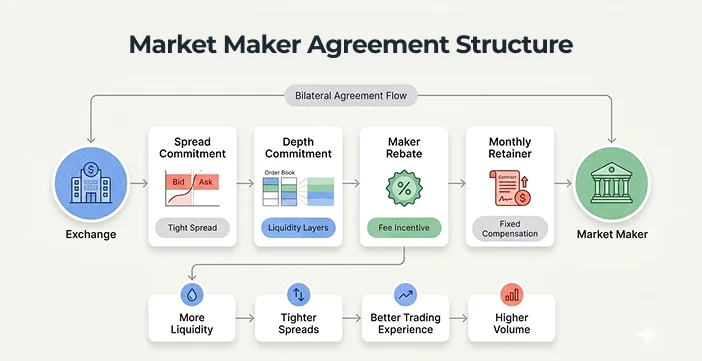

Professional market makers don’t show up because you have a good product. They need a formal agreement, and the terms determine whether you’ll get real depth or just a token presence on your book.

Wintermute, GSR, and DWF Labs evaluate three things before signing: your API quality, your fee structure, and your risk profile as a counterparty. Getting turned down by one of these firms on a first approach is common for new exchanges. Here’s what they’re actually checking.

API requirements. Your exchange needs a WebSocket feed with under 50ms order book update latency and a REST API supporting at least 100 to 500 requests per second for order placement and cancellation. Market making bots run on millisecond cycles. If your API throttles at 10 requests per second, that’s a non-starter for any serious firm before negotiations even start.

Agreement structure. A standard market maker agreement includes a minimum spread commitment (the firm keeps BTC/USDT spread under a specified threshold), a minimum depth commitment (typically $50,000 on each side within 0.5% of spot), and uptime requirements of at least 95% during active trading hours. In return, you offer a fee rebate and often a monthly retainer between $2,000 and $10,000 per pair, depending on the firm’s tier.

Revenue share alternative. Smaller firms will take a revenue share arrangement instead of a retainer. Usually 15% to 30% of taker fee revenue generated by the liquidity they provide. This defers your cash outflow and aligns incentives well: the more volume their depth drives, the more they earn. It’s a good structure for early-stage exchanges watching runway carefully.

Don’t approach Wintermute if you’re under $100,000 in daily volume. Their minimum engagement threshold is substantially higher. Start with regional or mid-tier firms, prove the volume, then escalate to institutional names with real data behind your pitch.

Passive vs Active Market Making for New Exchanges

Not all market making looks the same, and the right approach depends on where your exchange sits in its growth curve.

Passive market making means posting limit orders on both sides of the book at a fixed spread away from the midprice. A passive bot posts a bid at $0.50 below spot and an ask at $0.50 above spot, then waits for takers. It captures the spread, it doesn’t chase price moves, and it’s predictable enough to run without constant supervision.

Active market making adjusts quotes continuously as the market moves. When BTC drops $300 in 90 seconds, an active bot cancels resting orders and replaces them at new levels to stay competitive near the top of the book. This produces tighter spreads and a better trading experience but demands real inventory risk management and cross-venue hedging.

For day one of a new exchange, passive is safer. Active market making on a volatile pair without proper hedging can cost $5,000 to $15,000 in inventory losses during a single bad hour. We’ve seen this happen to teams that built their own algo without testing it against live market conditions. The math works in backtests. It doesn’t work during a 10% BTC move at 3am when nobody’s watching the dashboard.

The practical split: run passive on your top three pairs from the start. Let a professional firm handle active on BTC/USDT. Once daily volume stabilises above $1 million, consider layering active bots on additional pairs. But don’t rush that step.

Building a Market Making Bot vs Hiring a Professional Firm

You can build a basic market making bot in Node.js in two to three weeks. Whether you should is a different conversation.

A simple bot using your exchange’s REST API will post orders, monitor fills, and repost at updated prices. Inventory is managed with threshold rules: if the bot holds more than X BTC, pause the bid side; if it accumulates too much USDT, pause asks. This works reasonably well for low-volatility altcoin pairs in amounts under $50,000.

The cracks show during market events. When FTX collapsed in November 2022, any passive bot without hard stop logic started accumulating massive directional inventory within seconds. Exchanges running homegrown bots without circuit breakers saw their market making accounts lose $40,000 to $200,000 in under 90 minutes. That wasn’t a coding failure. It was the absence of risk controls meeting the wrong market day.

Professional firms bring co-location infrastructure, cross-exchange hedging, and real inventory management that a two-week Node.js project can’t replicate. If you’re launching with more than $500,000 in trading capital or targeting institutional users from the start, hire a firm. If you’re testing with $50,000 to $150,000 in liquidity capital and a small early user base, a basic passive bot keeps costs manageable while you build volume. Then bring in professionals once you have real numbers to show them.

The WebSocket and REST stack you’re already running on your exchange is sufficient to host a basic bot. Log everything from day one. Iterate on the threshold rules. Graduate to professional firms when the volume justifies the engagement size they need to take you seriously.

Liquidity Bootstrapping: Getting Real Depth Before Day One

The cleanest fix to the cold start problem is external liquidity aggregation. Instead of seeding your order book with your own capital and hoping for the best, you connect to an institutional liquidity provider like B2Broker, Leverate, or sFOX and stream their depth into your matching engine from launch.

This isn’t an AMM. An AMM uses algorithmic pricing through liquidity pools and works well in DEX environments. A CLOB exchange needs executable quotes from a real counterparty. External LP integration gives you that: users trade against a live institutional book via API, your matching engine sits in the middle and takes a spread on each fill. The LP doesn’t know your user. Your user doesn’t know the LP. You control the experience.

The integration work is real. You need a WebSocket connection to the LP feed, order routing logic, HMAC authentication, failover handling for disconnections, and a latency target under 100ms from user order to external fill. A competent backend team completes the core integration in two to four weeks. Get the failover logic right first. Sloppy disconnection handling means users getting fills rejected during LP outages at the worst possible time, and that kind of incident gets screenshotted and posted publicly.

Once the LP integration is live, layer on a liquidity mining program. Offer fee discounts or token rewards to users who post limit orders above a minimum size. Even $10,000 to $20,000 per month in incentives can move organic order book depth in months two through six. Most exchanges that successfully bootstrapped volume through 2024 and 2025 ran these programs for three to six months before organic depth was enough to hold on its own.

For a technical breakdown of what external LP API integration looks like at the code level, including WebSocket vs REST feed selection, failover architecture, and pre-launch testing, check out our external liquidity API integration guide for crypto exchanges.

Frequently Asked Questions

What is a thin order book in crypto exchange terms?

A thin order book means there are very few resting buy and sell orders near the current market price. The result is wide bid-ask spreads (often over 0.5% on major pairs) and significant slippage when a user tries to execute any meaningful trade size. A healthy BTC/USDT book on a mature exchange maintains $500,000 to $2 million of depth on each side within 0.5% of spot. Most new exchanges open with a fraction of that.

How much does it cost to hire a professional market maker for a new crypto exchange?

Retainer fees range from $2,000 to $15,000 per month per trading pair, depending on the firm and volume commitments. Mid-tier firms like Kairon Labs or Bluesky Capital typically start lower than Wintermute or GSR. Some accept revenue-share arrangements of 15% to 30% of taker fee revenue instead of a flat monthly fee, which works well for exchanges trying to conserve runway during the early growth phase.

What API specifications do market makers need from my exchange?

At minimum: a WebSocket feed with under 50ms order book update latency, REST endpoints for order placement and cancellation supporting at least 100 requests per second, and a sandbox environment for bot testing before going live. High-frequency firms also ask for FIX protocol connectivity and colocation options. Build the WebSocket feed first. It’s the blocker for most serious firms in the first conversation.

What’s the difference between passive and active market making for crypto exchanges?

Passive market making posts limit orders at fixed spreads and waits for takers. Active market making adjusts quotes in real time as market prices move. Passive is lower-risk and easier to operate but produces wider spreads. Active delivers tighter spreads and a better trading experience but requires real-time inventory hedging infrastructure. Most new exchanges start passive and graduate to active after volume stabilises above $1 million daily.

Can I use an AMM instead of order book market making for my new exchange?

AMMs and CLOBs serve different use cases. AMMs work well in DEX environments where professional market maker coordination isn’t feasible. If you’re building a CEX with a CLOB matching engine, external LP aggregation is the faster path to day-one depth. Some exchanges run a hybrid model, using AMM pools to supplement CLOB depth on long-tail altcoin pairs where professional market makers won’t commit capital. It’s a legitimate strategy for that specific use case.

How long does it take to bootstrap order book depth from zero?

With external LP integration, you can open with $1 million to $5 million in aggregated BTC/USDT depth on each side from launch day. Without it, organic bootstrapping through user activity and a liquidity mining program typically takes three to six months to reach reliably tradeable depth on major pairs. Most teams underestimate this timeline and open to users too early, which creates the exact first-impression problem they were trying to avoid.

What’s the standard maker-taker fee structure for attracting market makers in 2026?

Most competitive exchanges in 2026 offer maker rebates of -0.005% to -0.025% and taker fees of 0.05% to 0.1%. Tiered structures that reward higher-volume market makers with better rebates are now standard practice. Flat fee models without any rebate component struggle to attract professional liquidity providers who can get paid to post on established platforms. If your fee schedule doesn’t include a maker rebate, most serious firms won’t take the conversation further.