Most crypto exchange failures aren’t funding problems. They’re infrastructure problems that show up at 3am when volume spikes 40x and trades stop executing. Binance processed more than a million orders per second during the 2021 bull run. The system keeping that platform alive wasn’t the frontend or the mobile app. It was the order book matching engine — a piece of software most founders hand-wave past until it breaks.

If you’re building an exchange — whether from scratch, white label, or hybrid — this is the system that determines your latency, your fairness, and your survival at scale.

What a Matching Engine Actually Does

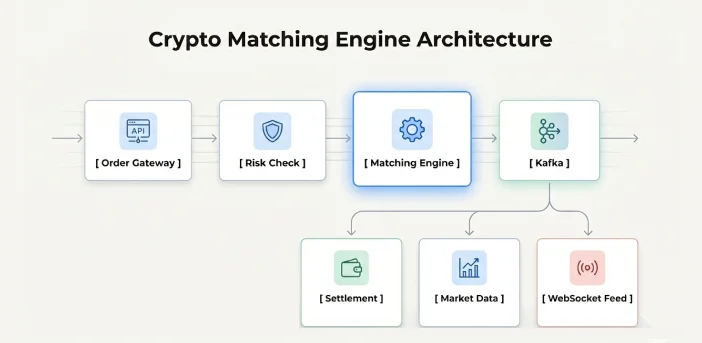

It’s not just trade execution. The matching engine is the coordinator of your entire trading layer.

When a user hits “buy,” the order travels from your API gateway through a risk check, into the matching engine’s order queue, and gets evaluated against the current order book state. If a compatible sell order exists at an acceptable price, the engine pairs them, publishes a trade event, and triggers balance updates downstream. If no match exists, the order rests in the book as a limit order, waiting.

That whole cycle runs in under a millisecond on a well-built engine. We’ve seen poorly architected engines add 40ms just in the order validation layer because someone built it over HTTP instead of a binary protocol. That’s the difference between attracting market makers and losing them to a competitor.

The engine also handles cancellations, order amendments, partial fills, and market data emission. It’s not a microservice. It’s the beating heart of your exchange, and every other system — settlement, risk, WebSocket feeds, reporting — depends on what it produces.

How the CLOB Works: Price-Time Priority and Bid-Ask Spread

A central limit order book (CLOB) is the data structure that holds all resting buy (bid) and sell (ask) orders, organized by price and time. Price-time priority means the engine always fills the best-priced order first. If two orders share the same price, the one that arrived earlier gets filled first. This is also called FIFO matching — first in, first out.

The bid-ask spread is the gap between the highest bid and the lowest ask. On a liquid exchange, that spread might be $0.50 on a Bitcoin pair. On a thin market, it can hit $50 or wider. The spread matters because it represents the real cost of trading for a market taker. Market makers earn that spread by providing liquidity. Takers pay it by hitting existing orders.

One thing founders miss: the CLOB is not just a sorted list. It’s a live, mutable state that needs to survive crashes, replay correctly after a restart, and stay consistent across distributed downstream services. Getting that right is where most DIY builds fall apart — usually around month seven when the team realizes the in-memory state and the database have quietly diverged.

The Data Structures Behind the Speed

Speed in a matching engine isn’t a configuration setting. It comes from the data structure you choose to represent the order book.

Two options dominate production systems. The red-black tree is a self-balancing binary search tree where insertions, deletions, and lookups run in O(log n) time. Most engines that need price levels kept in sorted order use a red-black tree — it rebalances automatically as orders arrive and cancel out. C++’s std::map and Java’s TreeMap are red-black trees under the hood. The skip list is a probabilistic alternative. It’s easier to implement with lock-free reads, which makes it attractive when you want concurrent access without a global lock. Some high-throughput engines built in Rust choose skip lists for exactly this reason.

For orders sitting at the same price level, each price node holds a FIFO queue. That queue is where time priority lives. So the full structure is two layers: a sorted tree of price levels, and inside each level, a queue of orders. This two-layer model is the standard CLOB implementation in every production-grade matching engine worth building on.

Matching Algorithms: FIFO vs Pro-Rata

FIFO is the default and the right choice for most exchanges. The first order at the best price gets filled first, full stop. It rewards aggressive quoting, it’s transparent, and traders can reason about queue position without a spreadsheet.

Pro-rata changes the rules. Instead of pure time priority, it allocates fills proportionally based on order size. If a 100-lot sell order arrives and two resting buy orders exist at the same price — one for 30 lots and one for 70 lots — pro-rata splits the fill 30/70. This model suits derivatives markets and options exchanges because it encourages large liquidity provision rather than speed-based queue gaming.

But pro-rata has a known problem. Traders inflate order size to claim a bigger proportional slice, then cancel the excess after the fill completes. One exchange we worked with chose pro-rata for their perpetual futures market. Within three weeks, order book depth looked ten times healthier than real liquidity. Actual fill rates on large IOC orders told a different story.

Hybrid models split the difference. Some engines apply FIFO above a threshold order size and pro-rata below it. dYdX v3 ran a FIFO off-chain matching engine with on-chain settlement — specifically to avoid per-transaction gas costs while preserving the price-time priority fairness model traders expected from a centralized venue.

Order Types That Matter for Your Exchange

You need, at minimum: market orders, limit orders, IOC, FOK, post-only, and stop orders. Each changes how the engine handles an incoming instruction, and missing one will cost you a category of traders.

A market order executes immediately at whatever price is available. It walks up (or down) the order book until filled or exhausted. Large market orders on thin books cause slippage. That’s not a bug — that’s market microstructure.

A limit order sits in the book at a specified price or better. It won’t execute until the market reaches it. IOC (Immediate-or-Cancel) fills whatever quantity is available right now and cancels the rest — it never rests in the book. FOK (Fill-or-Kill) is stricter: fill the entire order immediately or cancel the whole thing. Institutions use FOK to guarantee block fills without partial exposure.

Post-only ensures the order rests as a maker order only. If it would immediately match on arrival, the engine rejects it rather than executing it as a taker. On a maker-taker fee model, where makers earn a rebate of 0.02% to 0.05% on major exchanges, post-only matters enormously for professional desks running tight margin. Build it early. Market makers will ask for it before your first week of live trading.

Architecture: Language, Event Sourcing, and Kafka

The matching engine core should never touch a database directly. Production engines run entirely in memory. Persistence happens asynchronously through an event stream.

The standard pattern is event sourcing with a write-ahead log (WAL): every order action — placement, fill, cancellation — gets written to an immutable log before the engine processes it. If the engine crashes at 2am, it replays the log from the last checkpoint and rebuilds state. Apache Kafka is the industry-standard infrastructure for this. It acts as both the durable event log and the message bus for downstream services: your settlement system, market data broadcaster, WebSocket feed, and risk engine all consume from the same Kafka topics.

For language, Rust and C++ dominate serious production builds. Rust gives you memory safety without garbage collection pauses — and GC pauses are a real problem when you’re targeting sub-millisecond latency. A 10ms GC pause during a volatile market event is not acceptable. C++ has a deeper hiring pool and decades of production use in traditional finance. Go works well for exchanges targeting 10,000 to 50,000 orders per second — not institutional HFT performance, but more than sufficient for most crypto startups in their first two years.

Learn more about what separates a standard engine from an institutional-grade trading engine and the architecture decisions that drive that gap.

The LMAX Disruptor pattern is worth understanding. It’s a lock-free, ring-buffer-based concurrency design originally built for Java’s LMAX exchange, now ported to multiple languages. It eliminates mutex contention between producer and consumer threads — one of the main throughput ceilings in naive engine designs. If your engine stalls at 20,000 orders per second on hardware that should handle 10x that, lock contention is almost always the culprit.

Order Book vs AMM: When Each Model Makes Sense

AMMs (automated market makers) like Uniswap don’t use an order book. They price assets using a constant-product formula (x * y = k) against a pooled liquidity reserve. There’s no bid-ask spread in the traditional sense, but there is slippage on large trades and impermanent loss for liquidity providers.

Order book matching engines give you better price discovery for liquid markets. They support limit orders, which AMMs can’t do natively. And they attract professional market makers who prefer quoting at discrete price levels rather than providing passive pool liquidity.

AMMs win in two scenarios. First: long-tail asset markets where you can’t attract enough market makers to quote continuously. Second: fully decentralized infrastructure where you need trustless, non-custodial settlement on-chain without a central operator.

The honest split: if you’re building an exchange for established assets with real volume, build a CLOB. If you’re building a DEX for new or low-liquidity tokens, AMM or hybrid makes more sense. dYdX v3 is the clearest example of a hybrid that worked — off-chain CLOB with on-chain settlement, getting institutional matching speed without requiring users to trust a custodian with their funds.

Risk Controls You Can’t Skip

The kill switch shuts down the matching engine instantly. Not gracefully — instantly. You need this for runaway algorithms, compromised API keys, and fat-finger errors. Build it before your first beta user touches the platform. One exchange we know shipped without a kill switch. Their first market maker client had a config error that spammed 8,000 orders in four seconds. It took 11 minutes to stop manually.

Circuit breakers pause trading when price moves exceed a defined threshold in a short window — typically 5% to 10% in under 60 seconds on most major exchanges. They prevent flash crash cascades from turning a bad minute into an empty order book.

Self-trade prevention (STP) detects when a buyer and seller on the same account would match against each other and cancels one or both sides. Without STP, you create wash trading. Regulators treat wash trading as market manipulation, and it will surface in any serious compliance review. Every regulated exchange needs STP before launch.

Front-running prevention requires deterministic, timestamped order sequencing. Orders get timestamped on receipt and processed in strict sequence. Any deviation from that creates exploitable windows for co-located participants. Co-location is a legitimate service — charging institutional clients to place servers near your matching engine is standard — but it must be available transparently to all participants, not reserved for preferred partners.

Build, Buy, or White Label: Real Costs

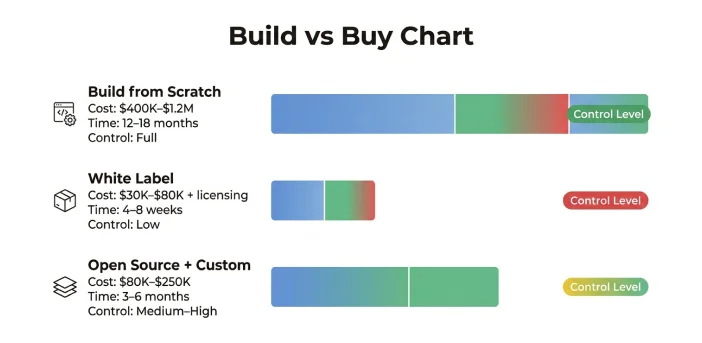

Building a production-grade matching engine in Rust or C++ from scratch takes 12 to 18 months with a team of 3 to 5 senior engineers. Total cost runs $400K to $1.2M depending on location, scope, and whether you need a FIX protocol adapter for institutional clients.

White label matching engines from vendors like AlphaPoint, B2Broker, or Modulus start around $30K to $80K for setup, plus ongoing licensing that typically runs $5K to $20K per month. You get to market in weeks. You give up control over performance tuning, custom order types, and anything your vendor’s roadmap doesn’t prioritize.

One exchange we worked with chose white label to save time. It worked for launch. Fourteen months in, they couldn’t add a custom order type their institutional clients needed. The vendor’s timeline was eight months. They rebuilt from scratch anyway — at full cost, with the added pressure of a live platform to maintain. Factor that into the decision early, not after signing a licensing contract.

| Approach | Typical Cost | Time to Market | Control Level |

|---|---|---|---|

| Build from scratch (Rust/C++) | $400K–$1.2M | 12–18 months | Full |

| White label (AlphaPoint, B2Broker) | $30K–$80K + licensing | 4–8 weeks | Low |

| Open source + custom (OpenDAX, HollaEx) | $80K–$250K | 3–6 months | Medium-High |

The open-source-plus-customization path is often the right call for well-funded teams that want control without starting from zero. Plan for 3 to 6 months of engineering to take an open-source base from “runs in staging” to “survives a 10x volume spike at 4am.” That gap is where most implementations need the most work.

Frequently Asked Questions

What programming language is best for building a crypto matching engine?

Rust is the best choice for new builds targeting sub-millisecond latency. It gives you memory safety without garbage collection pauses, which C++ doesn’t guarantee without careful manual management. Go is practical for exchanges expecting under 50,000 orders per second and wanting faster hiring and iteration. C++ remains the legacy standard in institutional systems where existing codebases exist.

What’s the difference between a CLOB and an AMM?

A CLOB (central limit order book) matches discrete buy and sell orders at specific prices using deterministic rules. An AMM (automated market maker) prices assets algorithmically against a liquidity pool using a formula like x * y = k. CLOBs support limit orders and price discovery. AMMs support passive liquidity provision and work without active market makers.

How many orders per second does a typical matching engine handle?

Performance varies by implementation. Consumer-grade exchanges typically process 50,000 to 200,000 orders per second. Institutional-grade engines built in C++ or Rust reach 500,000 to over a million. A well-tuned Go-based engine for a mid-volume crypto startup typically hits 10,000 to 50,000 orders per second comfortably.

What is price-time priority in a matching engine?

Price-time priority means the engine fills the best-priced order first. If two orders share the same price, the earlier order gets filled first. It’s the standard fairness model for spot crypto exchanges and rewards traders who quote aggressively or provide liquidity early in the queue.

How does event sourcing work in a matching engine?

Every order action — placement, fill, cancellation — gets written to an immutable event log (typically Kafka) before the engine acts on it. The in-memory engine state is rebuilt by replaying that log from the last checkpoint. This means crash recovery is deterministic and downstream services can consume the same event stream to stay synchronized.

What is self-trade prevention?

Self-trade prevention (STP) detects when an incoming order would match against a resting order from the same account or sub-account and cancels one or both sides. Without STP, the exchange creates artificial trade volume (wash trading), which regulators classify as market manipulation. Any exchange operating in a regulated jurisdiction needs STP before launch.

Should I build or buy a matching engine for my first exchange?

White label if your runway is under 18 months and you need live volume before you can raise again. Build from scratch if institutional clients are part of your go-to-market and you expect to need custom order types, co-location services, or FIX API integrations within your first year. The open-source-plus-customization path is often the best middle ground for well-funded teams that want control without starting from zero.